Interest rates in Switzerland have been rising for several months. Many factors are behind this rise, from central bank policies to the global economy. Therefore, it is important for consumers to understand the implications of this increase and how it may affect their ability to access consumer credit in Swiss. In this new article, we will examine consumer credit regulations in Switzerland, the evolution of interest rates, the impact of rising interest rates on loans and strategies to combat rising rates. of interest. We wish you a good reading!

How are consumer loan interest rates set?

Interest rates on private loans, depend on several stakeholders and several factors. Here is an overview of who does what before being able to determine the interest rates on private loans in Switzerland.

The Swiss National Bank and the Federal Council

Interest rates in Switzerland are determined by the Swiss National Bank but also by the Federal Council. The Swiss National Bank is responsible for setting the reference interest rate (policy rate). It is then used as the basis for interest rates on loans and deposits. For lending institutions, it is a question of carrying out financing operations at a lower cost. The objective is therefore to obtain funds as cheaply as possible and then lend them by generating a profit. The Federal Council sets the maximum interest rate applicable to consumer loans. These two rates are closely linked and influence the general level of interest rates on consumer loans.

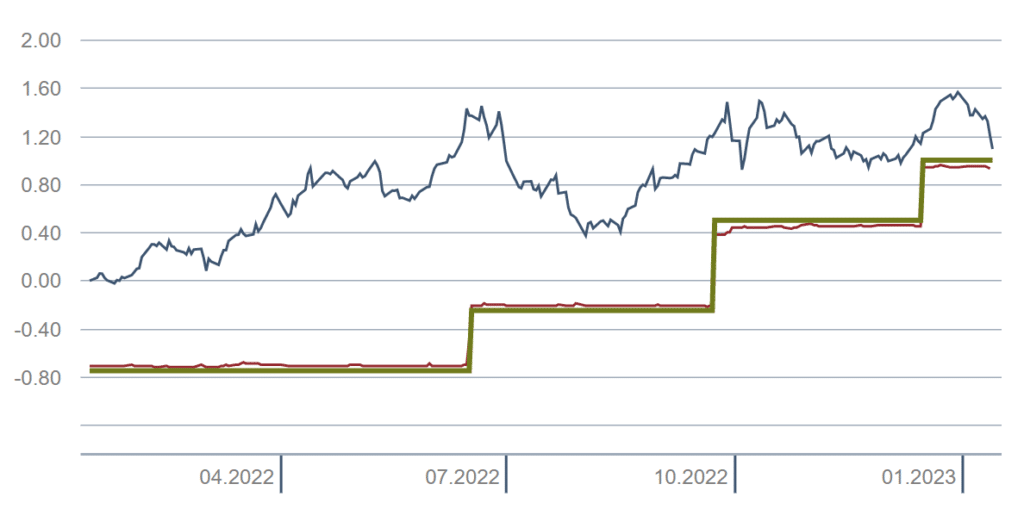

Here is the evolution of key rates over the last 12 months of 2022:

Lending institutions

Once the key rate and the maximum borrowing interest rate have been set, interest rates for loans consumption in Switzerland are then determined by the credit institutions themselves. This, according to their own interest rate policy and their credit risk. Interest rates may vary depending on the term and amount of the loan. But also depending on the financial situation and the risk profile of the loan applicant. Although very supervised, the activities related to private loans evolve in a very competitive market. It is therefore important for lenders to maintain the lowest possible rate offer.

FINMA regulations and ordinance of the Department of Justice and Police (FDJP)

Finally, it is important to emphasize that lending institutions are subject to cantonal regulations but also to the supervision of the FINMA (Federal Financial Market Supervisory Authority). Its mission is to protect the interests of consumers, maintain the stability of the Swiss financial system and monitor the best practices of lending institutions. The Federal Department of Justice and Police (FDJP), announces the maximum interest rate for consumer loans. This, according to the instructions of the Federal Council through the publication of an ordinance (see LCC and OLCC). So far, the maximum rate is set at 10 % for consumer loans and 12 % for credit cards. Taking into account the current rise in rates, it is very likely that these two rates will be readjusted in the months to come!

In summary :

The Swiss National Bank sets the key rate and the Federal Council sets the borrowing rate. According to these two reference rates, lending institutions can then determine the interest rates they will set on private loans. This taking into account different personal factors and the competition. At the same time, FINMA and the Federal Department of Justice and Police (FDJP), are keeping an eye on the grain to protect consumers and avoid overflows!

The effects of interest rates on consumer credit in Switzerland

Interest rates have a significant impact on consumer credit in Switzerland. When interest rates are low, it is easier for consumers to take out loans. They can indeed access credit at a lower cost. Conversely, when interest rates are high, it is more difficult for consumers to access credit because the cost of borrowing is higher.

Interest rates also have an impact on the amount of debt that consumers can contract. When interest rates are low, consumers can take on more debt because the cost of servicing debt is lower. When interest rates are high, it can be more difficult for consumers to access credit. This is because conversely the cost of servicing the debt is higher.

Recent evolution of interest rates on consumer credit in Switzerland

Interest rates on consumer loans in Switzerland are likely to increase significantly in the months or years to come. This is partly due to the policy of the Swiss National Bank, which increases the target rate. Its mission is to counter inflationary pressures in the Swiss economy. The Saron rate in Swiss francs has also risen steadily in recent months. This rise in rates will therefore have a direct impact on interest rates that consumers pay for their loans.

In addition to the policies of the Swiss National Bank, the recent rise in interest rates is also due to the global economy. For example, the US Federal Reserve increased its benchmark interest rate, which also had an impact on the economy in Switzerland. Therefore, interest rates on loans in Switzerland will certainly follow this upward trend.

Impact of rising interest rates on consumer credit in Switzerland

The rise in interest rates on consumer credit in Switzerland will have a definite impact on consumers. On the one hand, it will be more difficult for consumers to access credit, as the cost of borrowing will have increased. This is especially true for low-income households. They are more likely to see each other refuse credit because their ability to borrow is weaker.

In addition, rising interest rates will also impact the amount of debt consumers can take on. As the cost of servicing debt increases, many consumers will be forced to reduce their level of debt. This is in order to avoid default on their loans. This is likely to have a relatively large impact on the economy, as consumers will have to reduce their expenses.

Strategies for managing rising interest rates on consumer credit

Given the upcoming rise in interest rates on consumer credit in Switzerland, it is important that consumers are aware of the strategies they can use to mitigate the financial impacts.

One of the most effective strategies is to find the best interest rate. Different lenders may indeed offer different interest rates on consumer loans. It is therefore important for consumers to compare offers from different lenders in order toget the best terms. In addition, consumers should also consider redeem their existing loans, as it can help them reduce their monthly expenses.

It is also important for consumers to budget carefully. This can help them avoid taking on too much debt and defaulting on their loans. Consumers should also consider consolidate their debts. This can help them lower their interest payments by reducing the number of loans they have to manage.

A consumer credit in Switzerland remains an advantageous solution

Despite the increase in interest rates on consumer credit in Switzerland, taking out a loan still has many advantages. First, it can allow consumers to access funds they might not otherwise have access to. This can help them cover unexpected expenses or make a major purchase that they might not otherwise be able to afford.

In addition, consumer credit can also help consumers to improve their credit score. By taking out a loan and making payments on time, consumers can demonstrate to lenders that they are responsible borrowers. This can improve their chances of accessing credit in the future.

FAQ on the increase in interest rates for consumer loans in Switzerland

What is the cause of the rise in interest rates for consumer credit in Switzerland?

The main cause of the increase in interest rates for consumer credit in Switzerland is the policy of the National Bank which responds and adapts and the situation of the world economy. The Swiss National Bank has indeed increased its target rate and its discount rate in order to counter inflationary pressures in the economy. The US Federal Reserve also increased its benchmark interest rate, which also had an impact on the Swiss economy.

How can I deal with rising interest rates on my consumer loans in Switzerland?

There are a number of strategies you can use to manage rising consumer credit interest rates in Switzerland. Find the best interest rate can be a good option, as different lenders may offer different interest rates. You should also consider refinancing your existing loans and consolidating your debts to lower your monthly payments. Finally, a well-established budget can help you avoid going into too much debt.

Is it certain that consumer credit interest rates will increase in the coming months?

Presumably yes! However, it is still difficult to predict when this increase will take place. The only current certainty is the increase in the key rate and the borrowing rate is already being felt in our economy. A rise in consumer credit rates is therefore not an absolute certainty. However, it has a very high probability of materializing in the months or year to come. It is also not impossible that the rise in interest rates on private loans remains weak. This, because of the significant competition in this sector of activity. New players are seeking to position themselves and therefore force the various competitors to adapt their conditions in order to remain attractive.

Will I still be able to obtain credit easily in the years to come?

Access to liquidity through consumer credit will most likely remain an advantageous solution in the years to come. It is important to understand that no one would have an interest in making access to consumer credit impossible for the vast majority of consumers. Indeed, when they can borrow easily, they also spend more easily in our economy. It is important that consumers consume because it allows the economy to function. This stimulates production and creates jobs. Consumers who spend money on goods and services therefore stimulate the demand for these products. This then incentivizes companies to produce more to meet that demand. In sum, healthy consumption is essential to maintain stable economic growth. The various players will therefore do their utmost to maintain the attractiveness of consumer credit.

Our conclusion on the rise in interest rates in Switzerland

Interest rates on consumer loans in Switzerland will certainly increase in the months or years to come. This will have an impact on consumers, because it will be a little more difficult for them to access private loans. The amount of debt they can incur will also certainly be reduced. However, a common interest in maintaining a high level of consumption in Switzerland and the positive effects of a very competitive market should contain this increase. Consumers will therefore still be able to access consumer credit, but certainly in a more moderate way.

Prevention is better than cure…

At the same time, it is important that consumers are aware of the strategies they can use to manage these rising interest rates. Like finding the best interest rate and consolidating their debts. It is also important tosecure income whatever happens. By understanding regulations, the effects of interest rates, and strategies for managing rising interest rates, consumers can make informed decisions about their consumer credit. They make sure to get the best possible offers !

By requesting the services of Lica, you guarantee yourself significant savings by obtaining the best conditions on the market. Your credit specialist is there to guide you and help you make the right decisions. The earlier you start the process, the faster you will save money each month. By relying on the services from an independent intermediary like Lica, you will therefore have the certainty of being perfectly advised. You will thus benefit from the best private credit solution in Switzerland.

Do you have questions before applying for consumer credit? Our advisors are there to answer your questions 7 days a week directly on WhatsApp. Ask us for more information and we will be happy to answer you!